A recent Wall Street Journal headline boldly declared, “Climate Change Is Breaking Insurance.”

Earlier this year, in congressional testimony, the president of Aon emphasized that climate change is inducing “destabilization” within the insurance industry.

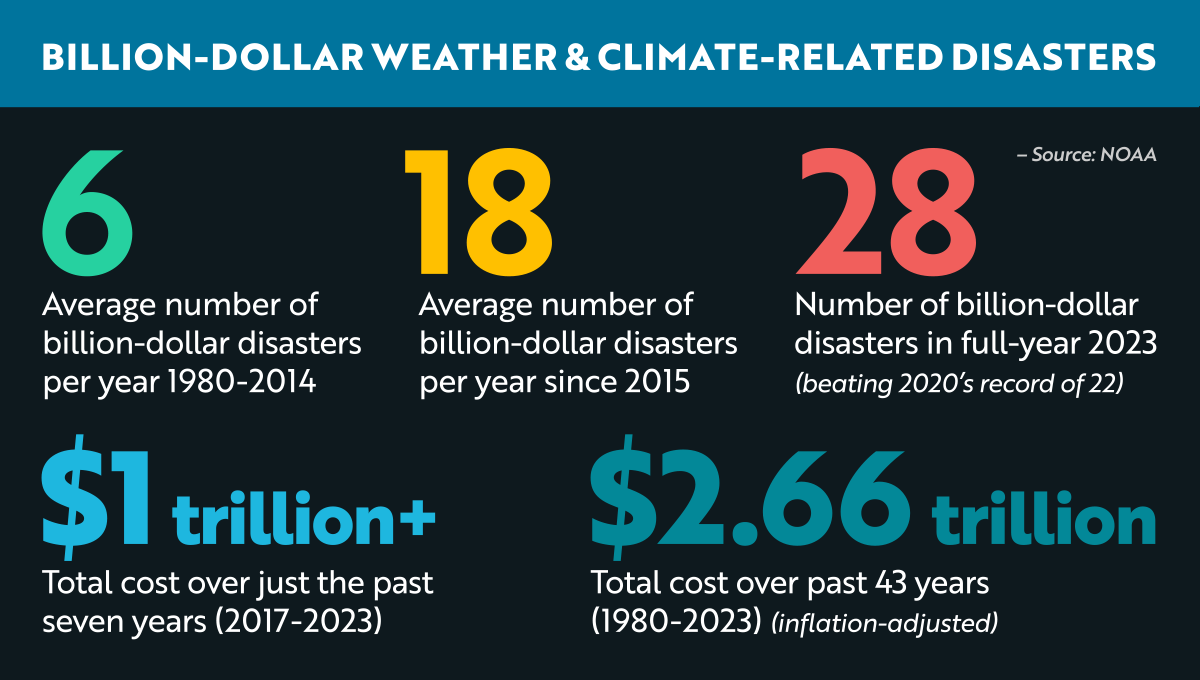

Total insured losses from weather-related natural catastrophes surpassed $122 billion last year, as reported by Swiss Re—markedly exceeding the historical average. Contrastingly, in the 1980s, the United States witnessed severe weather events, causing over $1 billion in losses every four months. According to the U.S. National Climate Assessment report, this frequency has escalated to once every three weeks.

“The rate of climate change has surged alarmingly,” warns the World Meteorological Organization (WMO). The UN Environment Programme called it a “code red” emergency for the world.

Amid these mounting concerns about the repercussions of climate change, the question arises: How can insurers fortify themselves against this challenge? How can they develop strategies to identify and mitigate associated risks?

While insurance inherently deals with risk, the escalating perils of climate change underscore the industry’s imperative to embrace technological innovation for effective risk mitigation. Here, we offer three immediate actions that Property & Casualty insurers can undertake. The encouraging news is that, in doing so, insurers have the potential to not only mitigate against their own risks, but contribute to the greater challenge of mitigating climate change risks for communities, consumers, and the world.

Action Item #1: Rethink Risk Assessment

Insurers can start this journey by rethinking their risk assessment processes. A report by the consulting firm McKinsey recommends that insurers use their annual policy cycle and their understanding of evolving risks to reprice and rearrange portfolios to avoid long-term exposure to climate events.

There’s just one problem: Insurers typically rely on historical data to calculate that future risk. But the climate system the industry has operated within over the past century is now gone. Traditional models and past loss experience just won’t cut it anymore.

Today, insurers need a far more current and accurate understanding of risk in order to price it profitably or avoid it altogether. Geospatial analytics is one technology that can help. When integrated with an insurance platform like Guidewire’s, for instance, solutions from companies like Betterview (recently acquired by Nearmap) and Cape Analytics leverage aerial imagery, computer vision, and predictive analytics to assess property risk instantly and on demand.

Guidewire’s HazardHub also analyzes and distills data from national sources to catalog risks that may damage or destroy property. It returns a risk score that insurers can use to determine whether they have appetite for a specific risk, and under what conditions.

To price and fund risk accurately, McKinsey says the industry will also need to invest in technologies that help them to understand the cascading effects of specific climate hazards on different sectors and geographic areas. Even when insurers decline to cover a specific property or facility, natural catastrophes that cause damage to infrastructures and supply chains can still impact those they do. According to Swiss RE, these knock-on effects could sap $23 trillion from the world economy by 2050.

Action Item #2: Deliver Innovative New Products

McKinsey points out that climate change also offers insurers an opportunity to create innovative new insurance products to cover newer and more frequent hazards, both acute (such as wildfires) and chronic (such as reduced crop yields).

Case in point: parametric insurance. Unlike traditional insurance, parametric coverage provides payment based on a triggering event (e.g., hurricane, earthquake, wildfire, or drought) of a set magnitude, instead of the value of physical assets. Technologies like those from Plover Parametrics and Demex enable insurers to manage parametric insurance while helping corporations identify and transfer risks to pre-certified carriers that act as “shock absorbers” for the threats emerging from climate change.

According to consultancy Marsh McLennan, parametric cover is particularly useful when there’s a lack of capacity or appetite from traditional insurance markets—especially where business interruption losses from a weather-related event are greater than the value of physical assets. For insurers, it’s an efficient way to not only mitigate risk, but streamline CAT response by automating payments at the exact time when the volume of claims being filed could overwhelm capacity.

Action Item #3: Help Businesses Mitigate the Risk to Us All

The UN report is dire in its estimation, concluding that there’s virtually nothing that can be done to avert the climate-related disasters caused by a 1.5° C increase in average global temperature expected over the next 20 years. But it’s not too late for nations and industries to drastically curb carbon emissions to stop temperatures from climbing even higher. The insurance industry can play a pivotal role in helping that happen.

New forms of pay-as-you-drive and usage-based insurance (UBI) policies, for instance, leverage smartphone-based telematics to reward consumers for driving less. The Usage-Based Insurance market is expected to reach almost $150 billion by 2027, with 25% yearly growth, according to Allied Market Research. This kind of coverage can be used to encourage the deployment of autonomous electric buses and trucking fleets that platoon to make transit safer and more efficient.

In fact, insurers can incentivize companies through more than just underwriting. According to Insure Our Future, the insurance industry is the second-largest institutional investor in the world, giving it enormous financial influence. On that score, Allianz, Aon, AXA, Munich RE, Zurich, and other major insurers are making strides in environmental, social, and governance (ESG) commitments to carbon neutrality in their own operations, as well as seeking similar commitments by the companies and funds in which they invest. Other insurers should follow suit.

From Risk to Resilience

The pressing “code red” emergency of accelerating climate change necessitates immediate action from insurers, not only to fortify themselves against escalating risks but also to contribute altruistically to the broader goal of mitigating climate change risks for communities and the world.

In navigating this ever-evolving landscape, insurers must initiate a fundamental reevaluation of their risk assessment processes, acknowledging the inadequacy of relying solely on historical data in the face of rapidly changing climate dynamics. Adopting technological innovations, including geospatial and predictive analytics, is becoming paramount in acquiring a more current and accurate understanding of risk. These strategic measures are essential in proactively addressing the mounting threats posed by climate change and extreme weather events, marking a significant step towards achieving industry resilience and supporting global risk mitigation efforts.

However, it is crucial to recognize that while urgently necessary, the trio of action items outlined here cannot single-handedly resolve the multifaceted threat posed by climate change. A collaborative approach involving national governments, mass awareness campaigns, regulatory mandates, and more is imperative. Only through concerted efforts on a global scale can we prevent the situation—already destined to be challenging—from worsening. The insurance industry’s commitment to technological innovation and risk mitigation serves as a vital component within this broader framework, contributing to a collective endeavor aimed at addressing the complex challenges presented by climate change.